Navigating the Storm: A Data-Driven Look at the 2007 Financial Crisis and Recovery Efforts

Introduction:

In 2007, the world experienced a financial shockwave that originated from the U.S. housing market downturn. The crisis quickly rippled across global economies, with significant impacts felt in the U.S., U.K., and China. In this post, we’ll explore a comprehensive analysis of the crisis and the concerted policy responses that helped navigate these turbulent economic waters. Accompanied by insightful Tableau visualizations, we delve into the monetary and fiscal adjustments that shaped the path to recovery.

The Epicenter of the Crisis:

The 2007 financial crisis is a stark reminder of the interconnectedness of global markets. Starting in the U.S., the collapse of the housing bubble sent shockwaves that were felt in the U.K., a major financial hub, and China, the burgeoning economic powerhouse. The crisis highlighted vulnerabilities and sparked a global debate on economic safeguards. Our Tableau visualizations, which I’ll share throughout this post, bring to life the data behind these seismic economic shifts.

Economic Indicators in Turmoil:

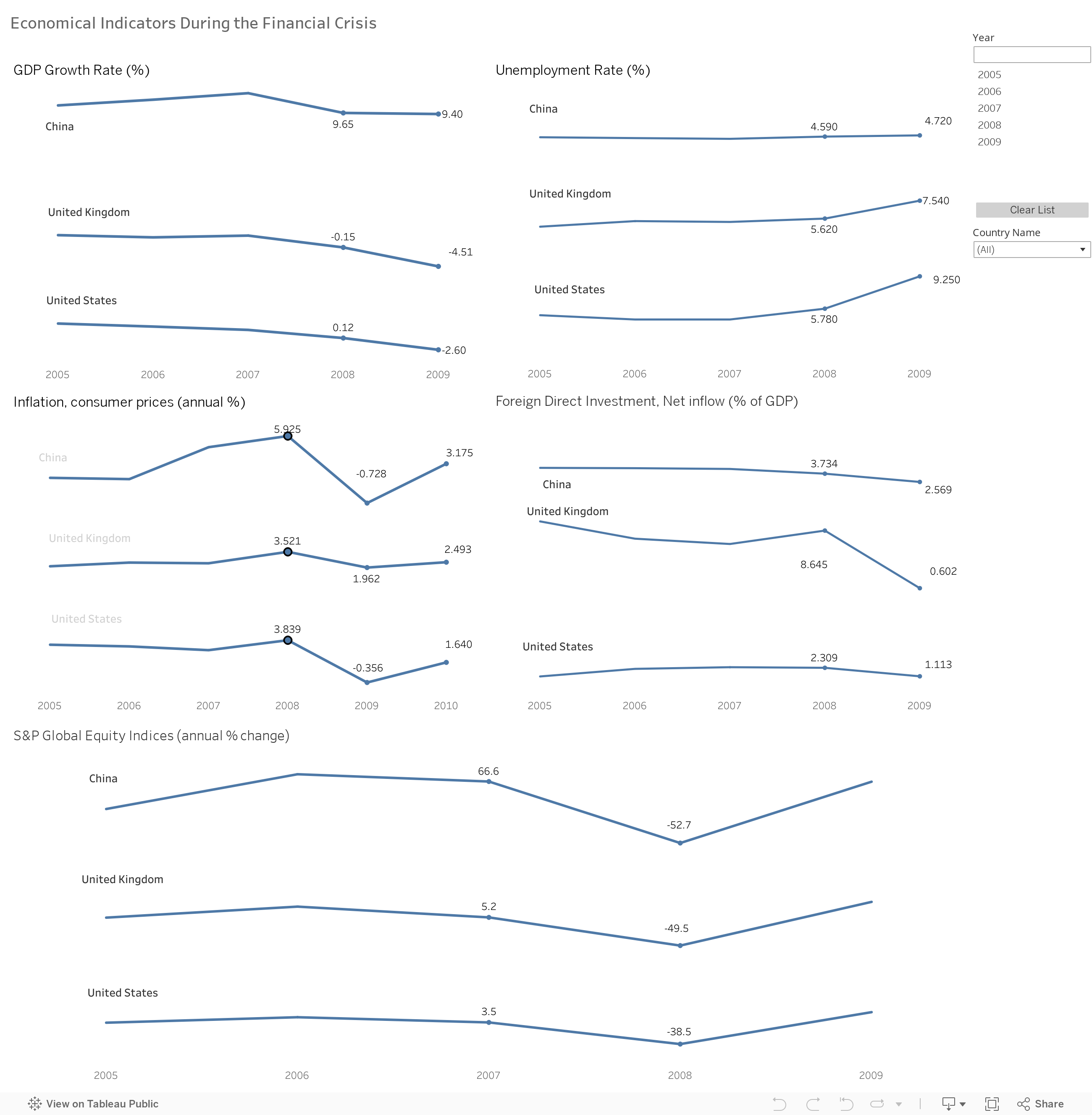

GDP Growth Rate: The severe downturn in the U.S. and UK economies in 2009, with GDP growth plummeting to -2.60% and -4.51%, respectively, signified deep recessions. China’s maintenance of a 9.40% growth rate, despite a global slowdown, demonstrated the effectiveness of its economic policies and a less interconnected reliance on global financial systems.

Unemployment: The dramatic rise in U.S. unemployment to 9.25% in 2009 mirrored the harsh reality of the economic crisis’s impact on the labor market. The UK’s unemployment rate’s more moderate increase to 7.54% indicated a resilient but strained job market. China’s steady unemployment rate suggested a controlled labor environment, possibly cushioned by government-led initiatives.

Inflation and Deflation: The pivot to deflation in the U.S. and China in 2009 highlighted the breadth of the economic contraction, marked by plummeting consumer demand. The UK’s decreasing inflation rate, from its 2008 peak, nonetheless remained positive, reflecting persistent cost pressures despite a contracting economy.

Investor Sentiment and Market Response:

FDI: The UK’s steep decline in FDI following the crisis suggested capital flight and a significant erosion of economic confidence, a contrast to the U.S.’s more stable investment climate. China’s gradual FDI decline mirrored the broader cautious stance of global investors during the period of uncertainty.

Equity Markets: The UK and U.S. equity markets’ deep dives of -49.5% and -38.5% in 2008, along with China’s -52.7% plunge, captured the panic and rapid revaluation of future earnings potential, significantly affecting wealth and spending.

Monetary & Fiscal Adjustments: Navigating Through Economic Turbulence

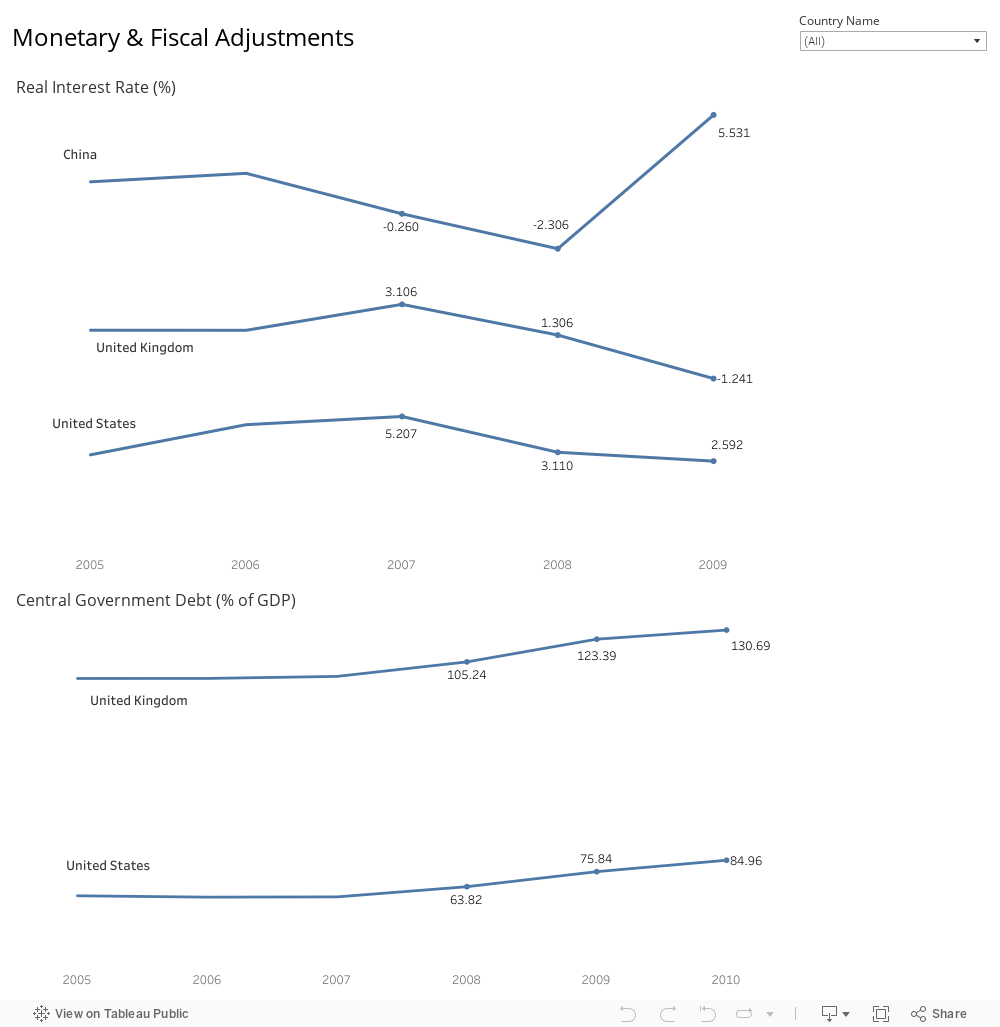

The global financial crisis of 2007-2008 forced countries to reevaluate their monetary and fiscal strategies. Central banks across the world slashed interest rates, while governments ramped up borrowing to inject liquidity and stimulate economic activity. The graphs provided offer a glimpse into how China, the United Kingdom, and the United States adjusted their policies in the face of economic headwinds.

Monetary Policy Adjustments: A Dive into Negative Real Interest Rates

In response to the financial crisis, China, the UK, and the US adopted aggressive monetary policies, including steering real interest rates into negative territory to encourage borrowing and investment. This is particularly evident in 2009’s negative real interest rates.

China responded to the crisis by lowering its real interest rates from -0.260 in 2007 to -2.306 in 2008, indicating a decisive move to encourage spending and investment.

The UK followed a similar path, with real interest rates dropping from 3.106 in 2007 to -1.241 in 2009, reflecting a substantial monetary stimulus.

The US saw its real interest rates decrease from 5.207% in 2007 to 2.592 in 2009, as part of its strategy to revive the economy.

Fiscal Stimulus: The Path of Increased Government Debt

The fiscal response to the crisis was marked by an increase in government debt, as seen in the upward trend of central government debt relative to GDP. This increase is indicative of a commitment to boost economic activity through government spending.

The UK’s central government debt rose sharply from 93.63% in 2007 to 130.69% in 2010, a clear sign of significant fiscal intervention.

The US also saw its government debt climb from 63.82% in 2007 to 84.96% in 2010, as it took on more debt to stabilize the economy.

For China, although not displayed on the graph, the World Bank and IMF data show an increase in central government debt from 16.4% in 2007 to 33.5% in 2010, demonstrating China’s use of fiscal policy to maintain economic momentum.

Analyzing the Impact of Policy Adjustments on Economic Indicators:

Following these adjustments, we look at how they influenced key economic indicators. The equity markets in all three countries showed signs of recovery in 2010, with China’s market increasing by 8.2%, the UK’s by 12.8%, and the US’s by 13.6%. Such improvements in the equity markets typically reflect greater investor confidence, potentially buoyed by lower interest rates making equities more attractive compared to fixed-income assets.

In terms of foreign direct investment (FDI), there was a noticeable uptick in all three countries. China’s FDI as a percentage of GDP went up by 55.9%, the UK’s by an impressive 345.2%, and the US’s by 57.7%. The growth in FDI highlights the global improvement in investor sentiment and market confidence, likely influenced by the monetary easing and fiscal stimulus measures.

As for GDP growth, all three countries experienced positive changes. China continued its robust growth; the UK and the US both rebounded from negative growth rates in 2009 to positive rates in 2010. These changes underscore the effectiveness of the stimulus efforts, which aimed to encourage borrowing, spending, and overall economic activity.

Findings and Recommendations:

The economic data from the 2007-2008 financial crisis reveal that while aggressive monetary easing and fiscal stimulus were critical in mitigating the downturn, the recovery trajectory varied significantly across nations. The U.S. and the UK, with deep contractions in GDP and spiking unemployment, required robust policy responses to revive consumer confidence and stabilize financial markets. On the other hand, China’s proactive fiscal measures, particularly in infrastructure, helped sustain its economic momentum. Our findings suggest that future crises may demand even more nuanced and sector-specific policy interventions. For instance, targeted support for small businesses and industries most affected by a downturn could provide a more efficient path to recovery. Additionally, policies aimed directly at consumers, such as mortgage relief programs, could prevent a cascade of defaults and stabilize the housing market more rapidly. A collaborative international response, leveraging the strengths of interdependent global economies, could amplify the efficacy of such measures. Therefore, we recommend a framework for economic policy that emphasizes flexibility, targeted support, and global coordination to not only cushion against immediate shocks but also to lay the groundwork for sustainable, long-term growth.

Conclusion: Steering Through Economic Adversity

The financial crisis that shook the foundations of global economies in 2007-2008 also brought to light the critical role of proactive monetary and fiscal policies in navigating economic adversity. The United States, the United Kingdom, and China each faced unique challenges and responded with tailored strategies that reflected their economic philosophies and priorities. Despite the varied approaches, the shared objective was clear: to stabilize the financial system, stimulate growth, and restore confidence. The recovery of equity markets, the resurgence of foreign direct investment, and the gradual uptick in GDP growth by 2010 are a testament to the effectiveness of these interventions. This period of economic recalibration provided valuable insights into the intricate dance between government policy and economic health, insights that continue to shape economic strategies in our increasingly interconnected world.