While one might expect to see better development outcomes after countries discover natural resources, resource-rich countries tend to have higher rates of conflict and authoritarianism, and lower rates of economic stability and economic growth, compared to their non-resource-rich neighbors. This is what has become known as the Resource Curse. Countries like Venezuela in Latin America, Angola in Africa, and Saudi Arabia and the United Arab Emirates in the Middle East have all exhibited varying degrees of this problem. Countries suffering from the resource curse also have significantly higher rates of pollution, and those with higher GDP per capita rely less on renewable energy sources. Because those countries are also mostly authoritarian, taxes are not collected from the people and government expenditures are not monitored.

In Lebanon, the prospect of commercial gas fields has excited the people and has led the government to sign contractual agreements with drilling companies to start exploring and producing commercial gas. Many believe that this project would enrich and stabilize Lebanon, but the history of resource-rich countries predicts otherwise.

Problem Evidence

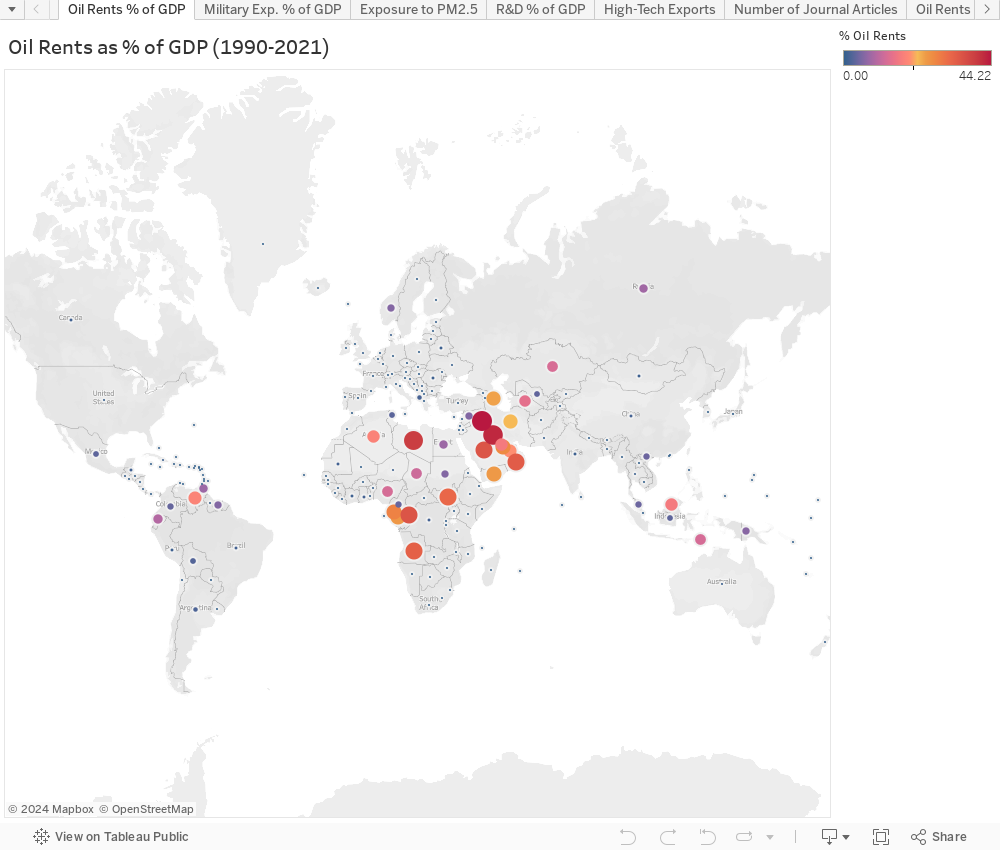

Economic Instability (related to SDG 8, 8.2): Below, we can see each country’s oil rents share of GDP, that is, the share of resource sales and exports out of total GDP. We can clearly observe that Gulf Countries and some resource-rich African countries like Libya, Angola, Democratic Republic of Congo and others, have oil rents account for 25 to 45% of their GDPon average for the past 30 years.

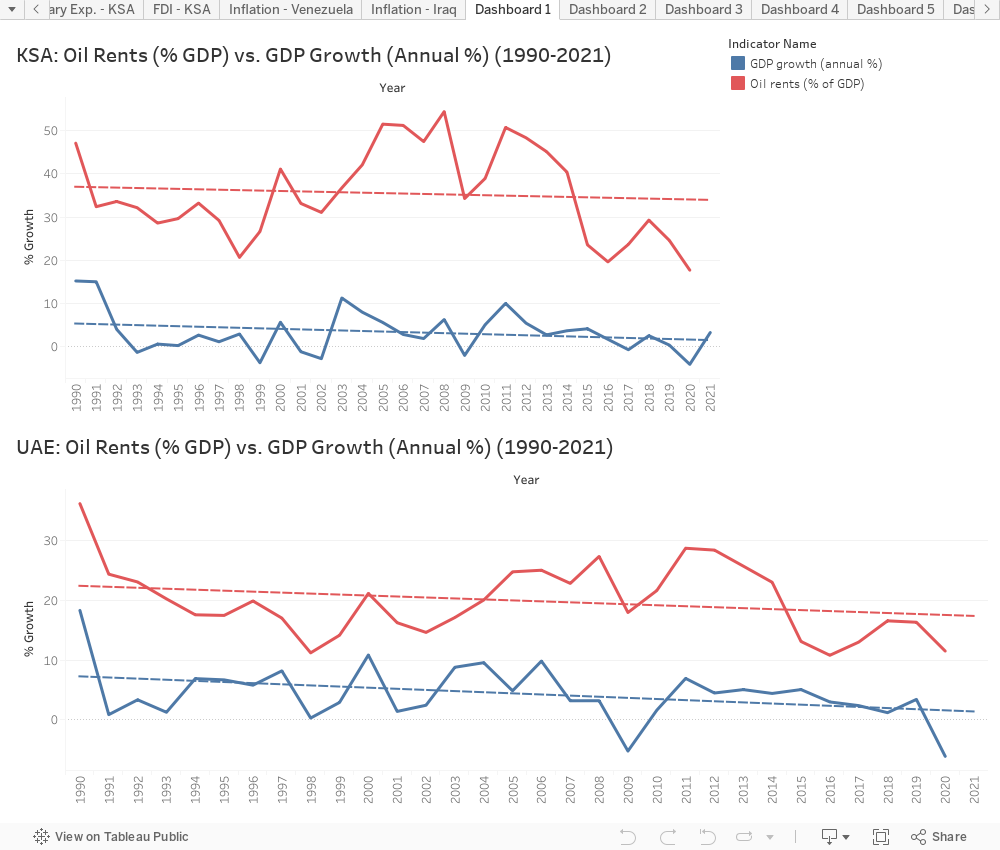

We can also see how Oil Rents move exactly in tandem with GDP Growth for Saudi Arabia and the UAE, which means that their economic growth is highly dependent on oil prices and sales volume, rendering it non-sustainable.

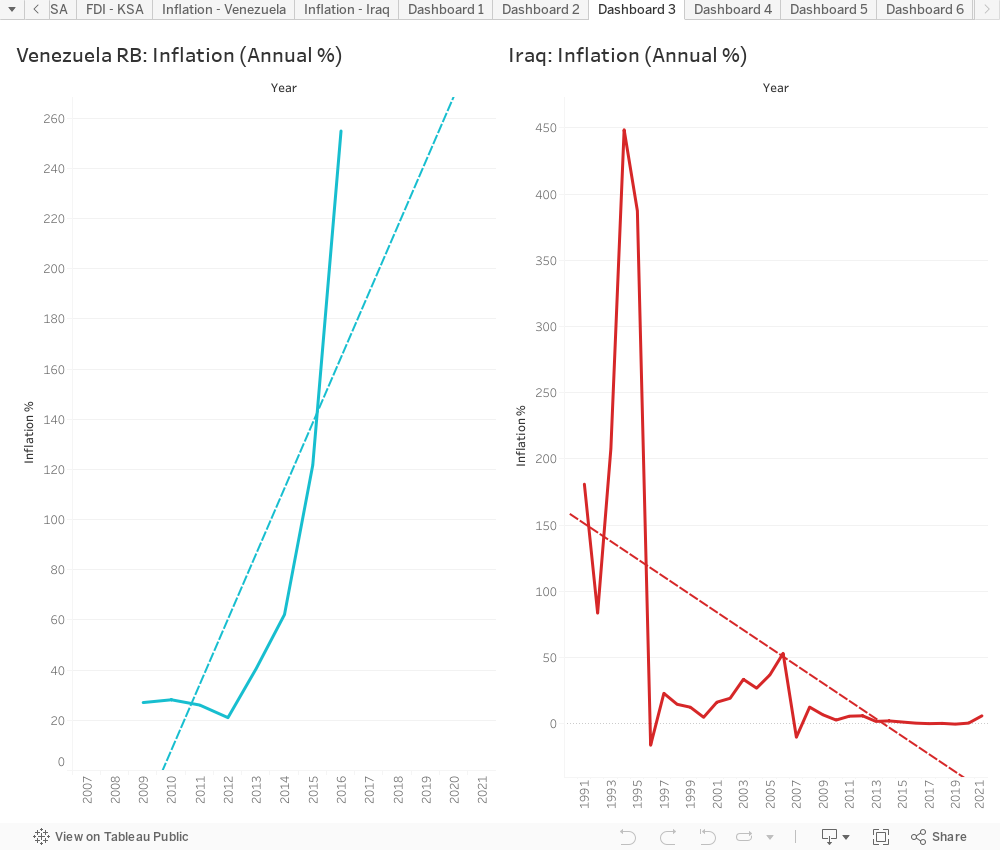

As for economic instability, severe inflationary periods have been recorded for these countries with the Gulf’s Oil Crisis in the 1970s through 1980s and the 1990 Oil Shock which impacted the Arab World greatly, and then Venezuela’s insane inflation rate which since 2016 has increased to 53,798,500%. These trends can be observed below for Saudi Arabia, the UAE, Iraq and Venezuela. The inflation rate is more volatile in these countries and the consumer price indices are in a steep upward trend.

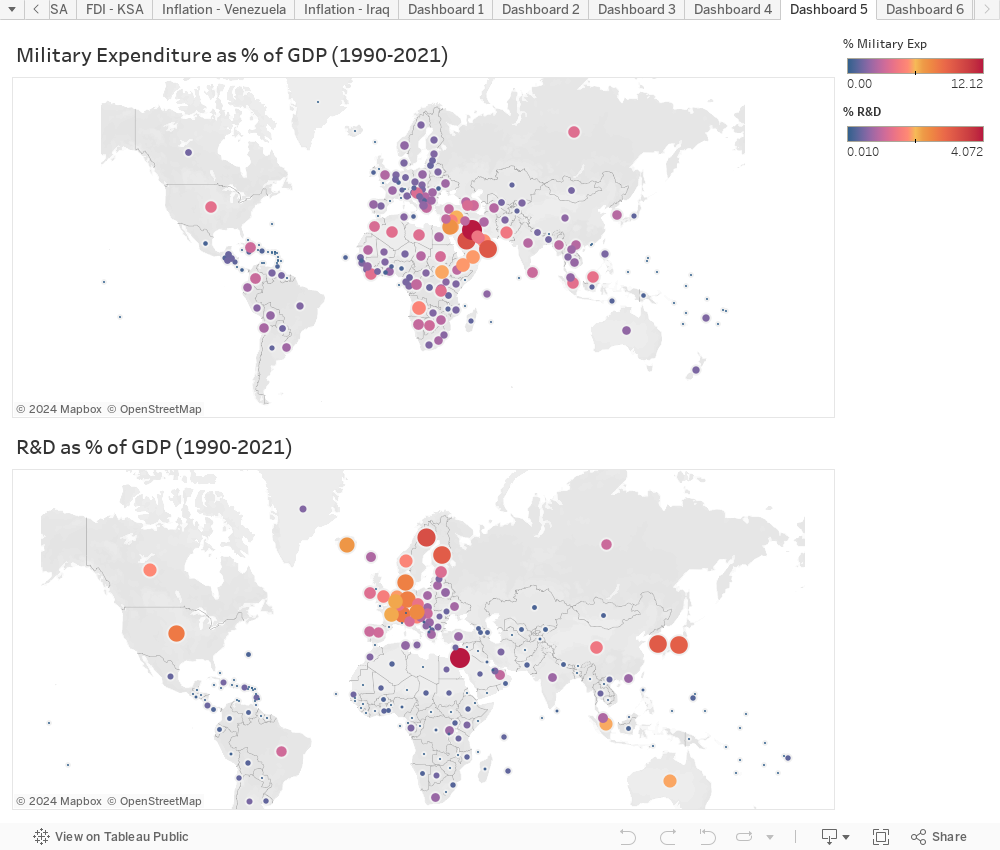

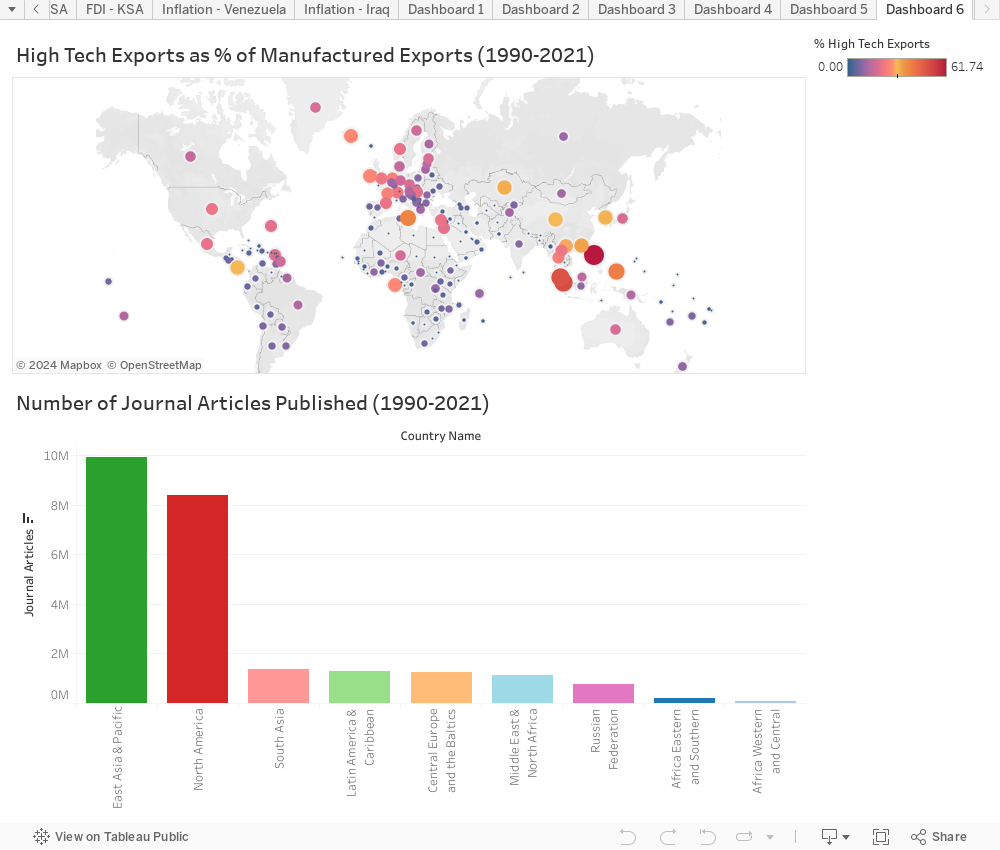

Conflict and Government Expenditures: We can see in the representation below how countries which were perceived to be most reliant on Oil Rents are also more likely to have a higher share of their GDP be dedicated to MilitaryExpenditure (SDG 16, 16.4). This indicates they are more prone to conflict, wars and social instability. Also, the lack of monitoring for governmental expenditures means that important sectors can be de-prioritized. For example, the research and development expenditures’ share of GDP is much lower in Arab countries than in Europe (SDG 9, 9.5, 16, 16.6).

The number of journal articles produced by each area of the world clearly shows the Middle East and Africa’s lower priority for innovation and scientific or scholarly research. High technology exports also have a low share of GDP in comparison with European, North American and East Asian countries.

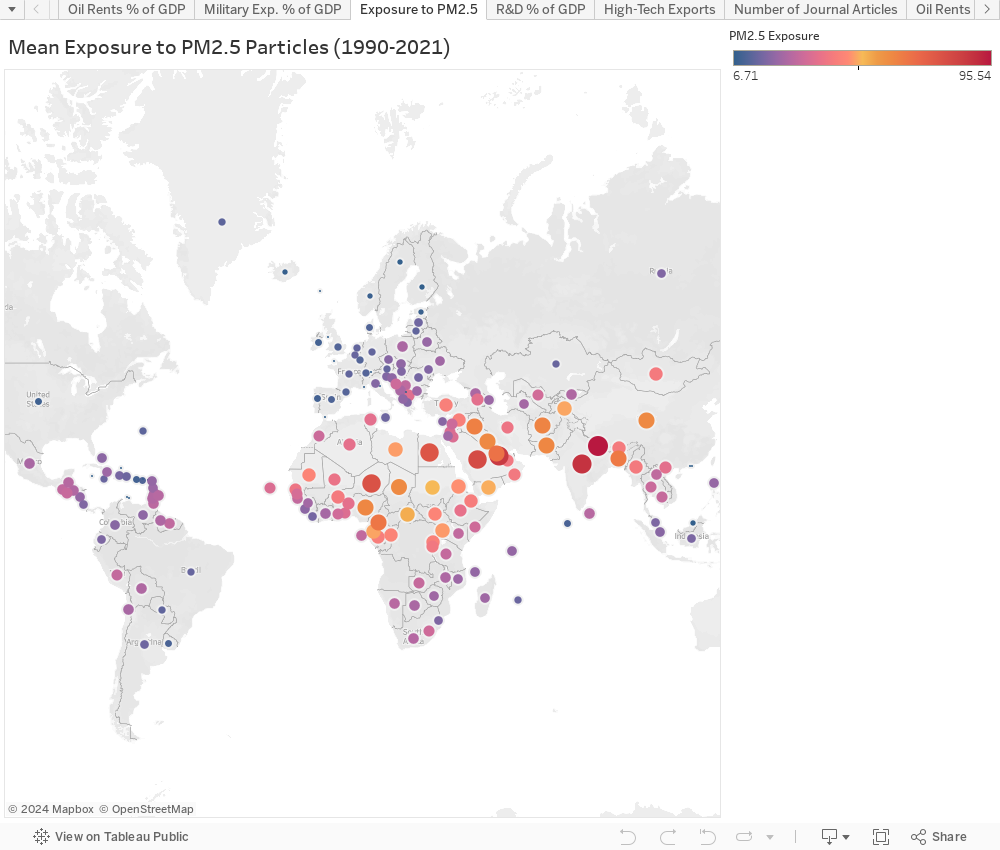

Pollution and Environmental Impact (related to SDGs 3, 7, 7.2, 8, 8.4): The mapchart below clearly shows the high exposure to PM2.5 molecules in resource-rich countries. Despite having lower population rates and less condensed cities, the Gulf Countries are amongst the most air polluted countries. Saudi Arabia uses only oil as an energy source and has a renewable energy sources rate close to 0% (out of total consumption). The UAE also uses only natural gas to power the country and no renewable energy sources.

Solutions and Reforms: Example of Saudi Arabia

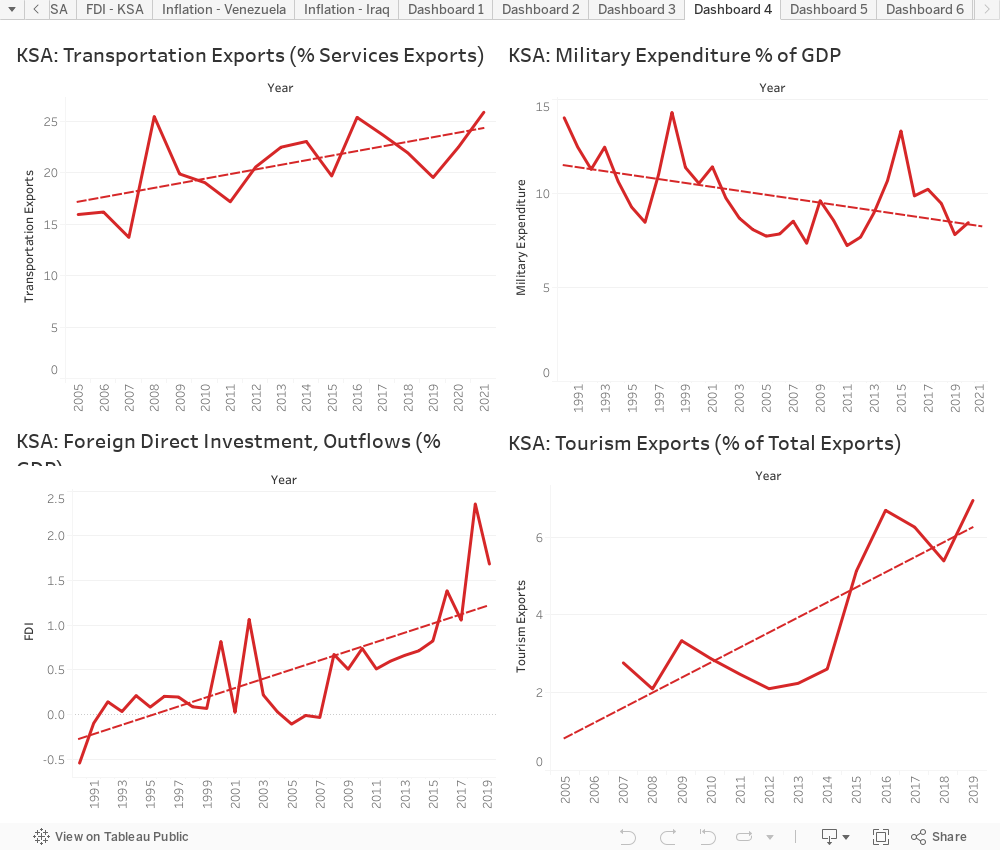

Eventually, Saudi Arabia took serious steps to diversify its economy and to become less reliant on its natural resources. It took counsel with the IMF during the early 2010s and then announced its Vision 2030 which aims for sustainable development and diversification of the economy. The data shows improvements on many levels. First of all, we can see that the GDP’s composition is shifting from being purely reliant on Oil Rents to including more activities done in the Transportation and Tourism (SDG 8, 8.9) sectors. We can also see that more Foreign Direct Investments are being made.The Military expenditures’ share of GDP is also regressing over time.

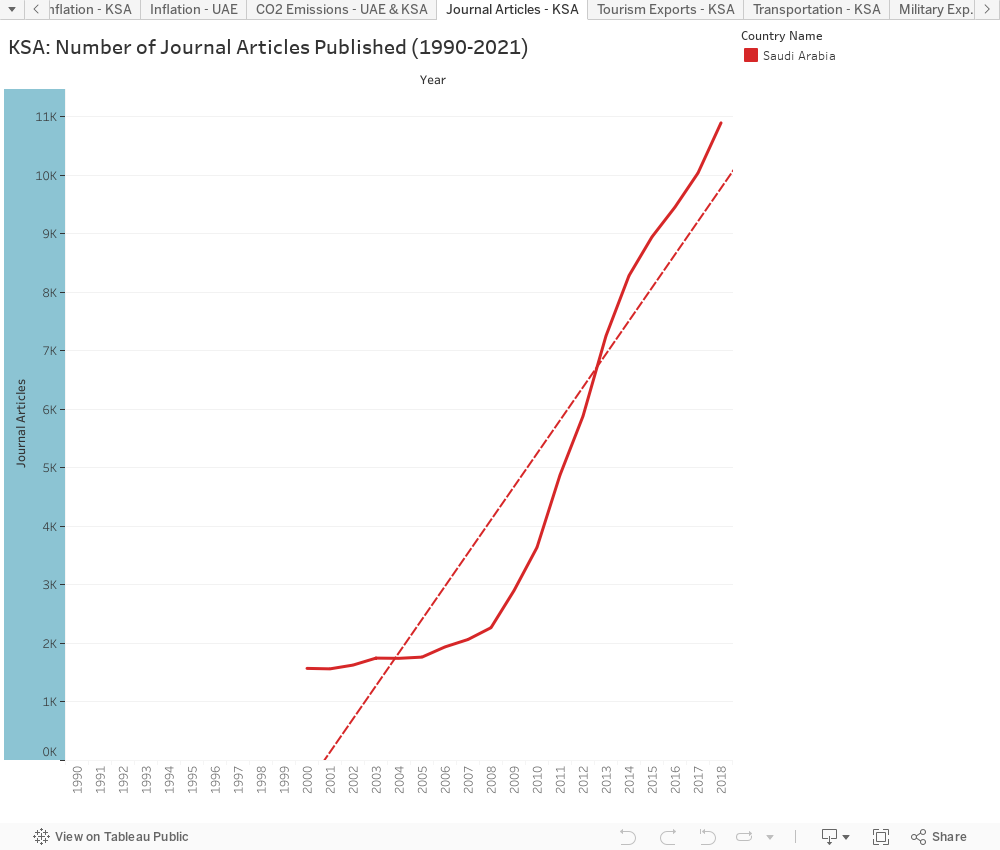

The number of journal articles published is also increasing rapidly with more and more Saudi Arabians focusing on scientific research and on new technologies (SDG 9, 9.5).

Recommendations for Lebanon

It is important to be aware of the consequences that a resource rich country may face by relying on its resource. Lebanon already has weak governance and is prone to economic instability and conflict, this is why it is especially important to learn about the reosurce curse and to keep encouraging the Lebanese people to be productive and to ensure that the governmental institutions are diversifying the economy, maintaining price stability, and producing energy from renewable resources even with natural gas being available as a resource; these concepts are especially relevant to the UN’s sustainable development goals which call for sustainable economic development, good governance, and environmental health. The data shows that proper public policy and budget controls can truly be impactful.

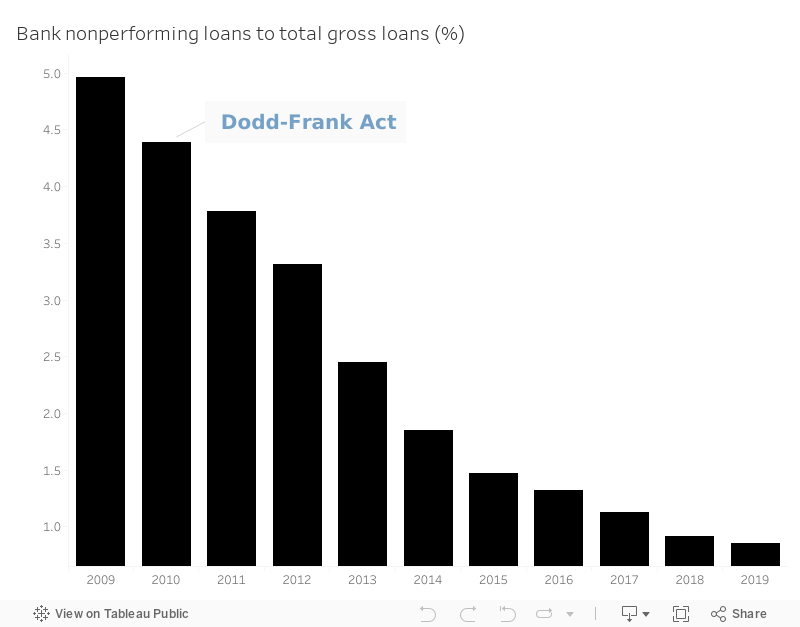

It wasn’t too long ago that Wallstreet was on the roll, but in reality, that growth was fueled by careless risk takings by the big banks. In the early 2000’s, the Federal Reserve heavily lowered the Fed Fund Rate, thus, cheap credit and NLPs (nonperforming loans) started taking place, allowing many consumers to borrow far more than they could afford. To understand what happened, we need to go just a few years back.

Let’s say you were a home buyer at the height of the market. Before you could get the house keys, you would have had to fill out a pretty big stack of mostly unintelligible mortgage documents from a big bank. This mortgage is essentially a debt note for the cost of the house. Now you might think that your bank would just put that debt note in a safe place while you went about making your monthly payments. But instead, that debt note took a little detour. Those loans got sold to other investors, which made big banks lose all incentives to avoid risks.

And as often happens when gamblers play with other people’s money, or money they don’t have, the big banks bet big, and lost big. And since the banks were so big, the entire economy got affected when they lost. Interest rates started rising back again, many subprime borrowers could not afford the higher rate as a result, millions went unemployed, small businesses couldn’t get credit, and the middle class got squeezed.

That brings us back to your nice new home. If you lost your job, you couldn’t make your mortgage payments. Worse, because of falling home values, you wouldn’t be able to sell it either without taking a big loss; putting you at risk of foreclosure by the big bank.

How did it end?

Wallstreet’s risky behavior had to be stopped. That was the purpose of the Dodd-Frank Wall Street Reform and Consumer Protection Act (2010).

The Act worked on preventing Predatory Mortgage Lending by:

Restricting some of the riskier activities of the biggest banks

Increasing government insight of banks activities

Forcing banks to maintain larger cash reserves

After the Dodd-Frank act, the percentage of nonperforming loans (NPL) to total gross loans started decreasing (Data Source: WDI).

Banks have been prevented from growing so large that they put the entire economy at risk if they were to fail. And if some financial firm still gets itself in trouble, despite the strong regulations, it will get shut down. No more bailouts.

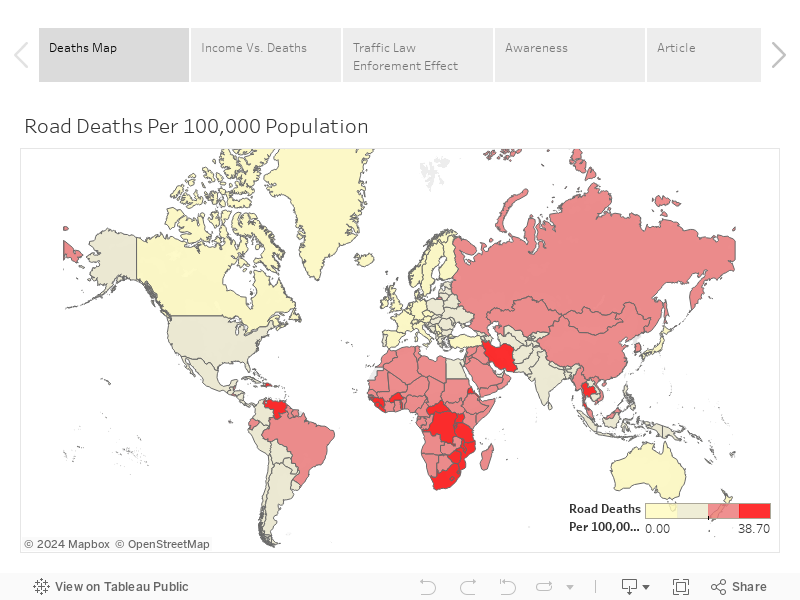

According to the Economist newspaper, in many countries where the overall mortality rate is falling, road deaths have gone in the opposite direction. Road traffic deaths disproportionately affect low- and middle-income countries that suffer from weakness in their roads’ infrastructure, where 90% of global road deaths occur.

You might think that it is only a matter of a nation’s income and its infrastructure expenditure! But, after harnessing the power of the data provided by World Development Index, it turns out poor infrastructure is only part of the problem. What’s interesting is that although the high income & oil rich Arab Gulf countries have world class roads infrastructure, the data shows that they still suffer from high road deaths. As a result of this insight, it can be deduced that the other reason behind the high road deaths is the rising incomes in many developing countries & cheap petrol prices have led to rapid motorization, while road safety management and regulations have not kept pace. In other words, their relatively weak enforcement of traffic laws, leads to risky driving, eventually higher road deaths.

In a nutshell, sophisticated roads’ infrastructure can’t effectively lower death roads on its own and should go hand in hand with strict traffic law enforcement.

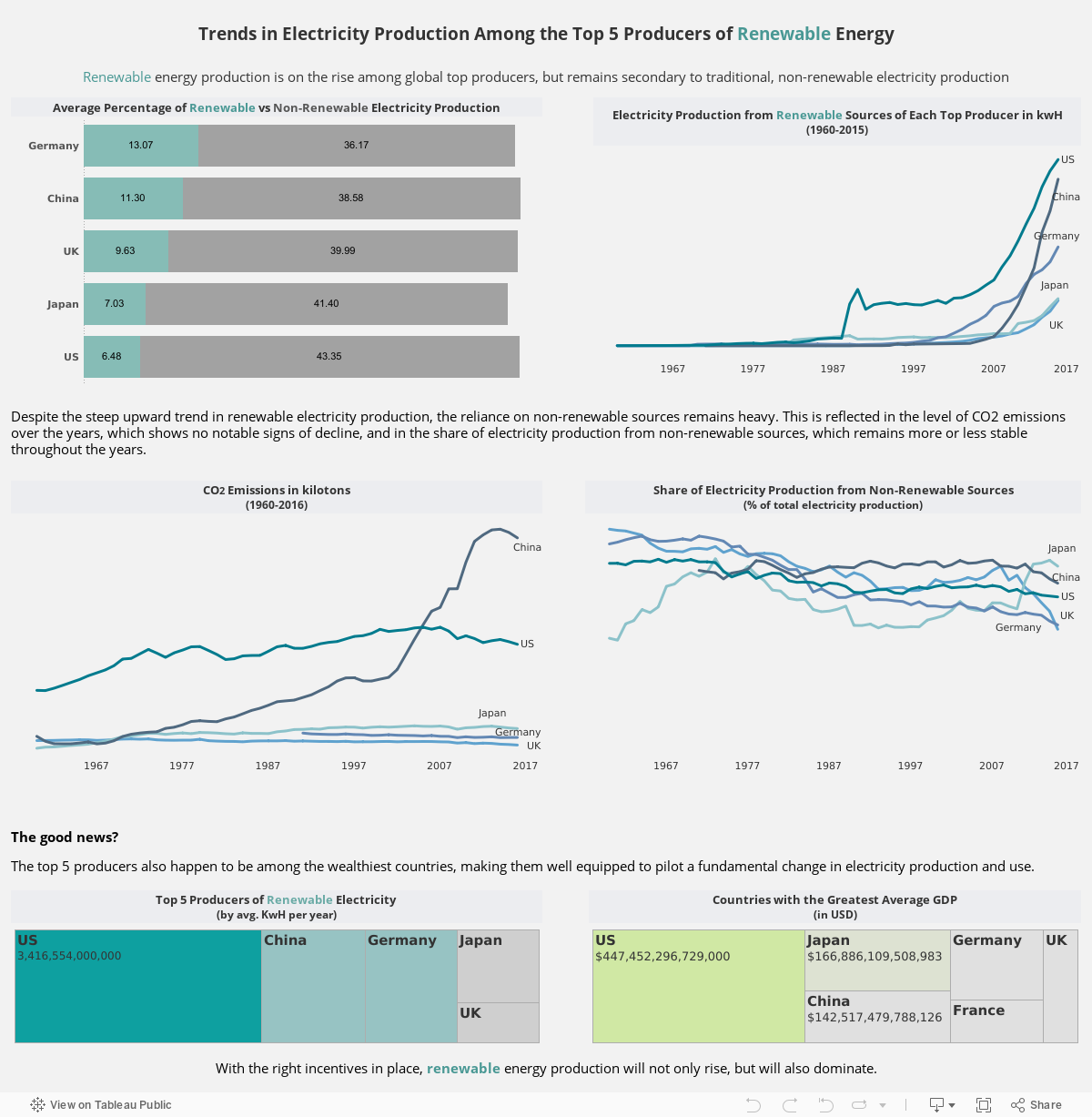

For the longest time, non-renewable energy production has been associated with power and wealth. While that remains apparent in the few nations that reap its bounty, another – uglier – side of the non-renewable energy production is coming more and more to light. Non-renewable energy production is the ultimate double edged sword: not only does it exhaust scarce natural resources, but it also results in greenhouse gas emissions that trap heat in the earth’s surface. As more non-renewable fuels are burned for electricity, our planet continues to heat, and a web of harmful reactions ensues.

The dashboard below explores trends in renewable electricity production among the top 5 producers of renewable energy. Compared to non-renewable energy, renewable energy produces minimal to no greenhouse gas emissions, making it an effective means to preserve natural resources, address global warming, and diversify energy supply.

Insights reveal that while renewable energy production is growing, non-renewable energy remains the main source of electricity production. To accelerate the growth in green energy production, governments must play a role in incentivizing its production and use, through anything from guaranteeing feed-in tariffs and providing interest free loans on setup costs, to further regulating CO2 emissions.

Local media outlets tend to praise Lebanon as the regional leader in entrepreneurship. Yet it seems that executives and board members tend to disagree with the headlines. They have openly criticized the media for spreading misconceptions, explaining that Lebanese start-ups struggle to sustain themselves due to governmental intervention, ancient business laws, and the absence of free economic zones. So I thought, why not harness the power of data to see where things really lie? Are laws interfering with Lebanon’s competitive ability? Using the World Development Index, Lebanon’s performance was evaluated through the number of governmental procedures required to register a start-up, and benchmarked with two of its main rivals: KSA and UAE. We observed the development of this metric over time from 2003 until 2019. Lo and behold, though it was the reigning champion a decade ago, Lebanon now significantly lags behind both its competitors. Lebanese Laws must be amended to streamline start-up registration procedures, or the country will be out of the race to assert itself as the regional entrepreneurial hub it once was.