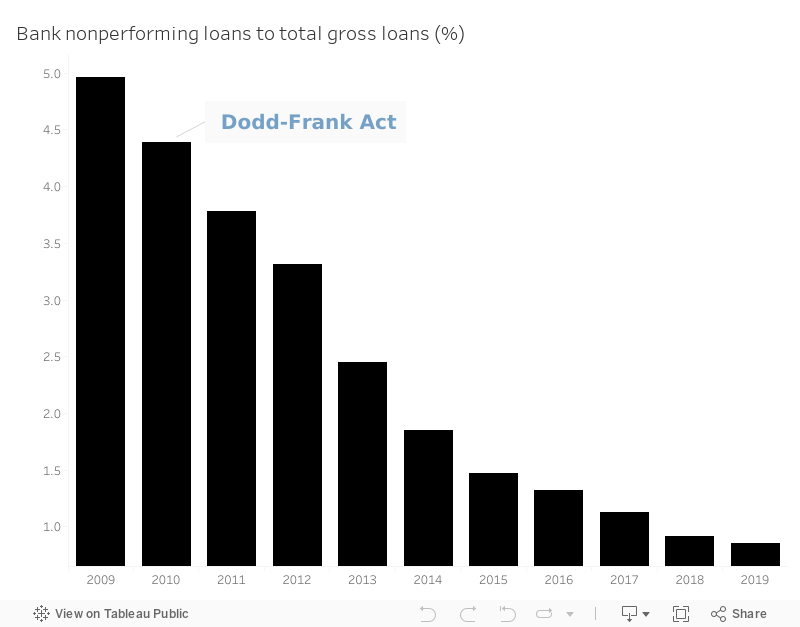

Banks Non-Performing Loans to Total Gross Loans in the US (2009-2019)

The 2007-2008 Financial Crisis

It wasn’t too long ago that Wallstreet was on the roll, but in reality, that growth was fueled by careless risk takings by the big banks. In the early 2000’s, the Federal Reserve heavily lowered the Fed Fund Rate, thus, cheap credit and NLPs (nonperforming loans) started taking place, allowing many consumers to borrow far more than they could afford. To understand what happened, we need to go just a few years back.

Let’s say you were a home buyer at the height of the market. Before you could get the house keys, you would have had to fill out a pretty big stack of mostly unintelligible mortgage documents from a big bank. This mortgage is essentially a debt note for the cost of the house. Now you might think that your bank would just put that debt note in a safe place while you went about making your monthly payments. But instead, that debt note took a little detour. Those loans got sold to other investors, which made big banks lose all incentives to avoid risks.

And as often happens when gamblers play with other people’s money, or money they don’t have, the big banks bet big, and lost big. And since the banks were so big, the entire economy got affected when they lost. Interest rates started rising back again, many subprime borrowers could not afford the higher rate as a result, millions went unemployed, small businesses couldn’t get credit, and the middle class got squeezed.

That brings us back to your nice new home. If you lost your job, you couldn’t make your mortgage payments. Worse, because of falling home values, you wouldn’t be able to sell it either without taking a big loss; putting you at risk of foreclosure by the big bank.

How did it end?

Wallstreet’s risky behavior had to be stopped. That was the purpose of the Dodd-Frank Wall Street Reform and Consumer Protection Act (2010).

The Act worked on preventing Predatory Mortgage Lending by:

- Restricting some of the riskier activities of the biggest banks

- Increasing government insight of banks activities

- Forcing banks to maintain larger cash reserves

After the Dodd-Frank act, the percentage of nonperforming loans (NPL) to total gross loans started decreasing (Data Source: WDI).

Banks have been prevented from growing so large that they put the entire economy at risk if they were to fail. And if some financial firm still gets itself in trouble, despite the strong regulations, it will get shut down. No more bailouts.