Why Startups Really Fail

If you’ve spent any time in the startup world, you’ve probably heard the usual explanations for failure:

“We ran out of money.”

“Bad timing.”

“Wrong hire.”

“Investors didn’t understand us.”

These reasons sound familiar because founders repeat them all the time. But when my team and I analyzed a dataset of more than 400 failed startups across multiple industries, a very different picture started to appear. The story of failure turned out to be much bigger than isolated mistakes or unlucky timing. It was deeper, more structural, and surprisingly predictable.

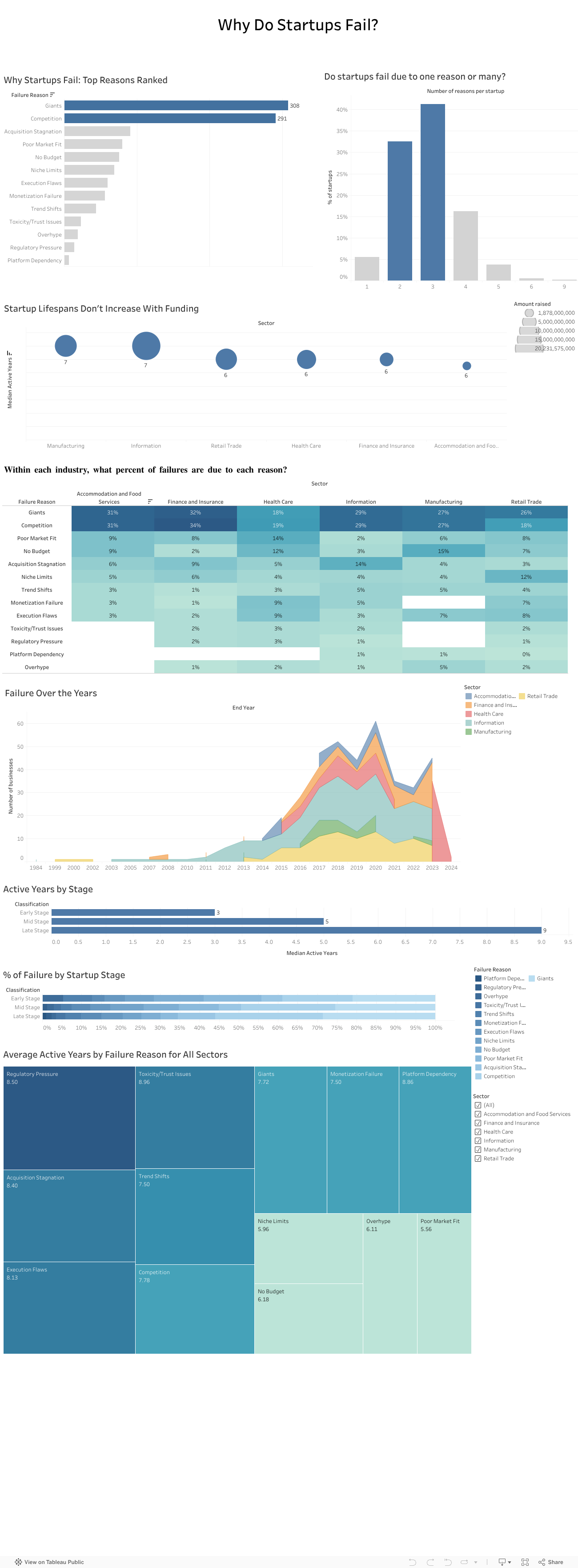

Failure rarely comes from one reason

One thing became clear very fast: startups almost never collapse because of a single issue. Most fail through a chain of events that build on one another.

In our dataset, about 40 percent of companies had three interconnected reasons behind their collapse. Sometimes a weak market fit slowed revenue and created cash pressure that left the company exposed to competitors. Other times overspending made the startup dependent on fundraising until investor sentiment shifted and the runway disappeared.

Either way, failure unfolded like a sequence of falling dominoes rather than one dramatic moment.

Competition quietly kills more startups than anything else

Across all sectors, competition was one of the most common reasons for shutdowns. And not just any competition. It was usually large, established players with strong distribution, deeper pockets, and loyal customers.

Nearly one in four failures mentioned competitive pressure. This confirmed what many founders experience but rarely quantify: good ideas often die quickly when the market is already controlled by powerful incumbents.

We tend to focus on product quality, team strength, and execution. Yet sometimes the biggest factor is simply how crowded or hostile the market is.

Your industry shapes how you fail

Another pattern that stood out was how differently failure plays out across sectors:

-

Healthcare startups struggled with regulation, slow adoption, and “no budget” barriers.

-

Tech and information startups were hit by rapid shifts in trends.

-

Retail and food startups faced thin margins, intense competition, and saturation.

So failure is not random. It is shaped by the environment each founder steps into from day one.

More funding does not mean a longer life

One of the most surprising findings was how little funding influenced survival. When we compared total money raised with lifespan, the relationship was almost flat.

Most startups survived five and a half to seven years, regardless of how much capital they had. Funding buys time, but it does not fix deeper problems like:

-

weak demand

-

slow adoption

-

dominant competitors

-

a misaligned business model

-

poor retention

This challenges a core belief in the startup world: raising more money does not automatically increase your chance of survival. The data simply did not support that.

What investors told us confirmed everything

To understand how investors themselves view these patterns, we surveyed 13 investment professionals. Their insights mirrored our data:

-

Competition was seen as the highest-risk factor.

-

Many felt the ecosystem lacked visibility and reliable signals.

-

They relied heavily on external sources to compensate.

-

Their top priorities were long-term growth and expansion potential.

Investors knew the risks, but they didn’t always have the tools to measure them consistently.

We also presented our findings to a company

To avoid analyzing the data in isolation, we presented our work to an investment company. Their feedback was striking. They struggled with the same issues many founders face, including unpredictable competition, unclear early-stage signals, and limited data visibility.

Our analysis helped them name challenges they had sensed for years but couldn’t articulate. It showed that this problem is not just academic. It is experienced daily in the ecosystem.

Where we go from here

The findings point to one clear conclusion: startups do not just need better products or stronger teams. They need a more realistic understanding of the terrain they are entering.

A stronger evaluation model would include:

- Deeper market and competition analysis

This means going beyond optimistic TAM slides and focusing on concentration levels, switching costs, and competitive power. - Sector-specific risk profiles

Every industry has its own patterns, barriers, and threats. - Stage-appropriate evaluation

Early-stage risk is not the same as late-stage risk. - A consistent and simple competition risk score

Something investors can use to compare opportunities objectively.

This type of framework is completely feasible with public data and existing tools. What matters is applying it early and consistently.

Final takeaway

Startups do not fail because founders are not capable or hardworking. They fail because they often walk into markets they were never equipped to survive in.

If founders and investors begin paying as much attention to market structure as they do to product and passion, the startup ecosystem could look very different. And maybe fewer great teams would disappear not because they failed, but because the game they tried to play was stacked against them from the start.

0 Comments